Next year, many companies will have a new compliance requirement.

Beginning January 1, 2024, the Corporate Transparency Act (CTA) will require that domestic US companies and foreign entities operating within the US disclose their Beneficial Ownership Information.

Under the CTA, companies will have to file their BOI report with the Financial Crimes Enforcement Network, or “FinCEN.” The timing of that report depends on when the company is formed:

- Companies formed prior to 2024 will have until January 1, 2025 to file an initial report.

- Companies formed after January 1, 2024, but before January 1, 2025, will have 90 days from formation to file an initial report.

- After January 1, 2025, new companies will have only 30 days to file the initial report.

There is no associated filing fee, and an attorney or accountant will not need to make the filings. Additionally, a company must file an updated report with FinCEN within 30 days of that company’s BOI changing. Unless BOI information changes, only the initial filing is required.

Filings will be made through an electronic, secure filing system available on the FinCEN website, which has not yet been rolled out.

Failure to comply with these requirements can result in criminal and civil penalties of $500 per day of noncompliance and up to $10,000, as well as up to two years of prison in extreme cases.

While we are not handling these filings on our clients’ behalf, we are happy to answer any questions companies might have about compliance with these requirements. To assist in that effort, below are some commonly-asked questions and clarifications:

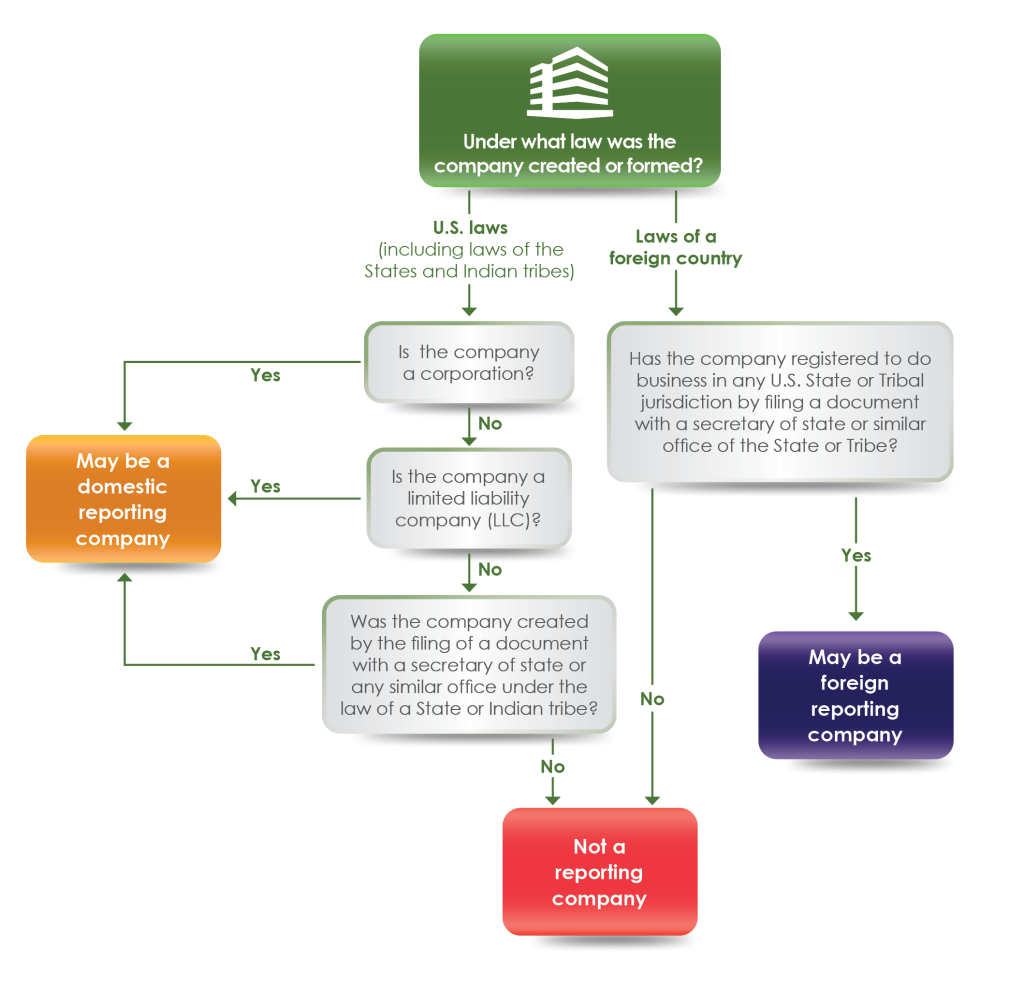

1. Who is required to comply with these reporting requirements?

FinCEN created a basic flow chart to determine whether an entity is considered a “reporting entity”:

In short, all US companies and foreign legal companies registered to do business in the United States must file unless a specific exemption provided by the statute applies. There are twenty-three exemptions outlined by the statute. Many of the exemptions apply to financial services companies, such as banks, investment firms, or financial advisors, or companies in other highly-regulated industries, such as governmental authorities, public utilities, accounting firms, or tax-exempt entities (including 501(c) non-profits).

Likely the largest source of full exemptions will come from the exemption for “large operating companies,” which requires that such companies:

- employ at least 21 full-time employees in the United States;

- have a physical office in the United States; and

- have more than $5 million in gross receipts or sales in the previous year from sources in the United States.

If an entity does not fall under one of the statutory exemptions and operates in the United States in any capacity, it must comply with CTA requirements.

2. What information needs to be reported?

The entity must report its:

- Legal Name

- Any trade or “doing business as” names

- Street address of principal place of business

- Jurisdiction of formation or organization; and

- Tax identification number.

Additionally, it must report the following information for each beneficial owner:

- Legal name

- Date of birth

- Current residential street address

- Identification number from an acceptable form of identification, such as a driver’s license, passport, or local identifier. Regulations state a disfavor of foreign passports where another acceptable form is available; and

- An image of the identification form described in #4.

3. Who is a beneficial owner?

A beneficial owner is any individual who, directly or indirectly, exercises “substantial control” or owns or controls at least 25% of a reporting company’s ownership interests.

An individual exercises “substantial control” if the individual:

- serves as a senior officer of the company;

- has authority over the appointment or removal of any senior officer or a majority of the Board of Directors; or

- directs, determines, or has substantial influence over important decisions made by the reporting entity.

Accordingly, senior officers and other individuals with significant authority over a company’s operations are likely considered beneficial owners under the CTA, regardless of whether they have an actual ownership interest in the entity, and regardless of their formal title.

4. Is there any alternative to disclosing this personal information?

Rather than routing personal information through these initial and updated reports, individuals can submit their personal information to FinCEN directly and obtain a “FinCEN identifier.” Individuals can submit that identifier as part of initial or updated reports in lieu of that individual’s personal information. In theory, FinCEN is receiving the same personal information either way, but this may limit the number of forms where that personal information appears and might mitigate the potential for reporting errors or leaks.

Companies anticipating a compliance burden under the CTA may want to begin requesting that their beneficial owners obtain FinCEN identifiers now to facilitate a simpler and more private filing process.

5. Who has access to BOI information?

To dovetail with the intention of the CTA, submitted BOI information can only be obtained by government bodies for national security, intelligence, and law enforcement purposes, as well as financial institutions in limited circumstances. BOI information will not be publicly available. State, local, and tribal authorities requesting this information will need a court order, and financial institutions conducting legally required due diligence may only obtain it with customer consent. Foreign law enforcement bodies may obtain this information through their partnerships with United States federal agencies.

For additional information, a few additional resources have been provided below:

- Corporate Transparency Act Full Text

- BOI Frequently Asked Questions – FinCEN

- Small Entity Compliance Guide [PDF]– FinCEN