Classifying your workers correctly is important not only for your business’ finances but also for legal liability. Employment and labor laws affect different types of workers in different ways, and they are also taxed in different ways.

What’s an employee?

The IRS typically assumes workers are employees unless stated otherwise. Employees are workers who are paid as salaried or hourly and may be subject to overtime. They’re taxed based on their income and as a business, you must withhold federal income taxes, state income taxes and FICA taxes (Social Security and Medicare) from them. They receive a W-2 form from the business showing their annual income every year after filling out a W-4.

If you have employees, your business must also make payroll and FICA tax payments.

Employees generally receive better treatment under labor laws than contractors. For example, state law generally requires employers carry workers’ compensation insurance to compensate employees injured on the job. Employers generally must carry unemployment insurance. Employers must abide by the Fair Labor Standards Act and the Department of Labor’s rules on overtime. In some states, employees must be entitled to take meal and rest breaks during shifts. Contractors do not receive these benefits.

What’s an independent contractor?

An independent contractor is a worker outside of the business. They are “independent” meaning they might run their own business or also do work for one or more other businesses. A contractor is hired by a company to perform specific work for the business. Typically, a contractor is given a discrete project or set of tasks to complete with minimal direct supervision.

Contractors do not have to have federal or state income taxes or FICA taxes withheld from the amounts paid to them. Independent contractors are responsible for all of their own income taxes, including self-employment taxes. They fill out a W-9 and receive a 1099 form from the business showing the total amount they’ve been paid by the business every year if the payment totals over $600.

If you have contractors, you don’t necessarily have to make payments for FICA taxes. Many employment and labor laws also do not apply to independent contractors, but they do apply to employees.

How to distinguish between the two

The IRS, DOL and the courts each have a test for determining whether a worker is a contractor or an employee. Per the overview provided by the IRS, there are three main rules to help distinguish whether your worker is an employee or a contractor:

-

Behavioral: Does the company control or have the right to control what the worker does and how the worker does his or her job?

-

Financial: Are the business aspects of the worker’s job controlled by the payer? (these include things like how worker is paid, whether expenses are reimbursed, who provides tools/supplies, etc.)

-

Type of Relationship: Are there written contracts or employee type benefits (i.e. pension plan, insurance, vacation pay, etc.)? Will the relationship continue and is the work performed a key aspect of the business?

Businesses must weigh all these factors when determining whether a worker is an employee or independent contractor. Some factors may indicate that the worker is an employee, while other factors indicate that the worker is an independent contractor. There is no “magic” or set number of factors that “makes” the worker an employee or an independent contractor, and no one factor stands alone in making this determination. Also, factors which are relevant in one situation may not be relevant in another.

This, of course, is just an overview. The actual test is much more complex.

If you’re still not sure, ask yourself these questions:

- does the company control or have the right to control what the workers does and how the worker does the job?

- are there written benefits for the worker like a pension plan, health insurance, paid time off or vacation pay?

- is the worker paid a consistent, set amount of money for their services?

- does the company manage how the worker is paid, reimburse for expenses or provide tools and/or supplies?

- does the worker primarily do their work in the employer’s place of business?

- is the relationship assumed to be permanent?

If most of the answers are yes, it’s likely that the worker in question is an employee. If you’d like to talk more about the differences, contact us. Note that misclassified employees can make a business liable for backed employment taxes, tax penalties, backed overtime and potentially civil remedies. For more on misclassification issues, you can also check out this infographic by the DOL.

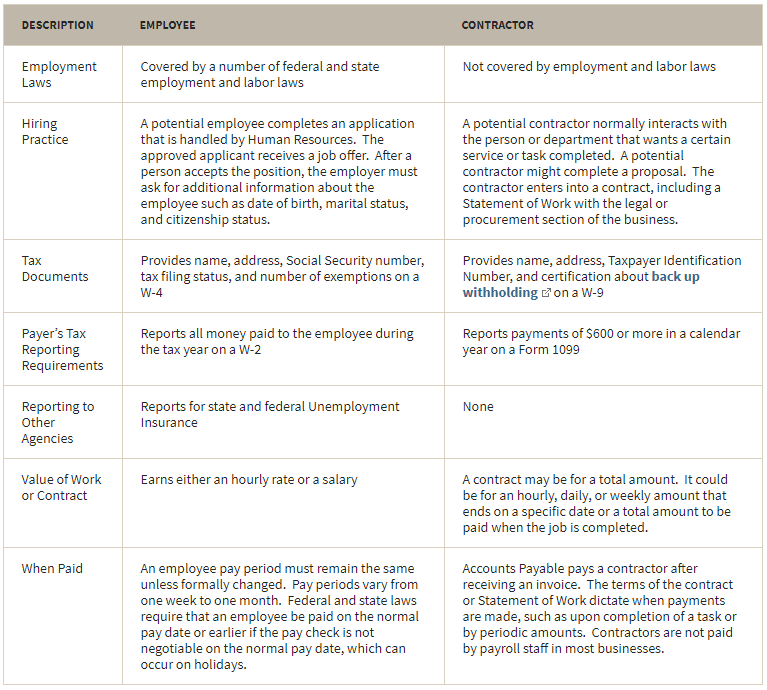

And here’s a great table also provided by the government as an overview of the differences between contractors and employees:

It’s critical to remember this: just because a contract says a worker is an independent contractor does not mean that they are. The IRS, DOL and the Courts will look at the actual relationship between the parties, not just the contract.

View all posts by this author

Comments are closed.